On July 1, a major update to Reg CC – the Federal Reserve Bank’s official rules for check clearing – takes effect, meaning some important changes are in store for how financial institutions handle paper and images. Many of the updates are simple revisions to the language of the rules, to account for the fact that most checks are now cleared electronically, rather than in their original paper form. Others, however, have the potential to impact day-to-day banking operations for many FIs around the country.

On July 1, a major update to Reg CC – the Federal Reserve Bank’s official rules for check clearing – takes effect, meaning some important changes are in store for how financial institutions handle paper and images. Many of the updates are simple revisions to the language of the rules, to account for the fact that most checks are now cleared electronically, rather than in their original paper form. Others, however, have the potential to impact day-to-day banking operations for many FIs around the country.

As a scanner manufacturer, we mainly concern ourselves with the parts of the regulation that involve the capture and handling of images. (It is worth mentioning that all of our product lines offer models that meet the new Reg CC endorsement recommendations.)

Below, we will attempt to answer the following questions related to Reg CC and check image capture:

- Are physical endorsements now mandatory on all checks I receive through remote deposit capture (RDC)?

- How do the Reg CC changes affect liability for duplicate deposits?

- What are the new ‘restrictive endorsement’ guidelines for check deposits? Is there anything specific that needs to be printed in the endorsement?

- What’s the difference between the word “endorsement” that I’m used to, and the word “indorsement” used in Reg CC?

- Do the endorsement guidelines affect liability for all types of fraud, or only duplicate deposits?

- Do the Reg CC endorsement guidelines apply to all check images, or just those accepted through RDC?

- Does a virtual endorsement meet the liability standards in Reg CC?

- How is mobile check capture affected by the Reg CC endorsement changes?

- Will I need to replace check scanners because of the new regulations?

Please be aware that these are only general talking points intended to help you gain a basic understanding of the new regulations. We are not attorneys or compliance officers, so please do not treat this as legal advice – when in doubt, ask a professional in those fields! Note also that there are other changes to Reg CC that affect things like funds availability requirements, returned-item procedures, and more, but those are not discussed here.

No, it is still up to the bank whether it wants to require an endorsement or not. The new Reg CC merely suggests that endorsements be used due to important changes in the way liability is handled in the case of duplicate deposits.

Under the old rules, if someone deposited a check at two different banks (usually, once through RDC and a second time by taking the physical paper check somewhere else), it was first-come, first-served. The bank that processed and cleared the check first got paid, and the second bank was on its own to recover whatever money it had paid out.

Under the old rules, if someone deposited a check at two different banks (usually, once through RDC and a second time by taking the physical paper check somewhere else), it was first-come, first-served. The bank that processed and cleared the check first got paid, and the second bank was on its own to recover whatever money it had paid out.

The usual way to do this was to simply take the funds back from the customer. If the money was already gone, however – as was often the case in deliberate fraud events – then the second bank was often stuck with a loss.

The new rules change this by putting the responsibility on the first bank that receives the check (or image of the check) to make sure that everyone else knows it has already been deposited. When there is a duplicate deposit under the new Reg CC, it is effectively an either/or situation:

- If the paper check did not have a physical endorsement, then the second bank to accept it can make a claim against the first bank for failing to take reasonable precautions;

- If the paper check did have a restrictive endorsement, the second bank to accept it cannot make a claim, because it should have known better than to accept a check that had already been endorsed to another institution or by another means of deposit (i.e., electronically).

The regulators directly state that their reasoning was to “place appropriate incentives on the parties best positioned to prevent multiple deposits of the same item.” In almost all cases, that’s going to be the first bank that receives the check for deposit.

Importantly, the regulation does not specify that the first bank in a duplicate deposit situation HAS to be held liable if it failed to require a restrictive endorsement. Financial institutions are free to reach their own private agreements about how to handle losses, and the second bank in duplicate deposit situations is not required to file a claim over the lack of a restrictive endorsement. However, the original bank is indemnified if it did require the restrictive endorsement.

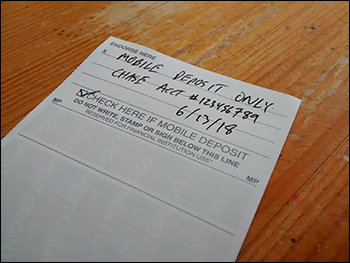

In plain English, the guidelines merely suggest that checks accepted via remote deposit should be physically endorsed in a way that would be difficult to mistake if the original paper check was later (accidentally or deliberately) deposited at another bank. There is no specific language required, although the guidelines give examples such as: “For mobile deposit only at XYZ Bank, date, and account number.”

In plain English, the guidelines merely suggest that checks accepted via remote deposit should be physically endorsed in a way that would be difficult to mistake if the original paper check was later (accidentally or deliberately) deposited at another bank. There is no specific language required, although the guidelines give examples such as: “For mobile deposit only at XYZ Bank, date, and account number.”

The key language, in our opinion, is that the second bank involved in a duplicate-deposit situation cannot make a claim against the first bank “if it accepted an original check containing a restrictive indorsement that is inconsistent with the means of deposit.”

In the example used above, there are four pieces of information that could potentially indicate that the check has already been deposited somewhere else: 1) a different bank name; 2) a different method of deposit; 3) a different date; and 4) a different account number. The rule doesn’t specify which, or how many, of these indicators would constitute sufficient “proof” in the event of a dispute, but if we had to guess at its intention, it would be that you should include as many pieces of information as possible, so that there can be no mistake at all.

Would an endorsement with one piece of information – i.e., only the bank name, or only “for mobile deposit” – be sufficient? Maybe. But what if two banks shared similar names, or if the duplicate was the result of someone submitting the check through mobile deposit at two banks? Then the outcome is less clear. Better to be safe than sorry.

For reference, most of our scanners with single-line endorsers can accommodate up to 90 characters. So a typical endorsement containing all four pieces of information, such as …

FOR REMOTE DEPOSIT ONLY, FIRST NATIONAL BANK, 06/18/2018, ACCOUNT 123456789

… would fit with about 15 characters to spare. In almost all cases, it should be possible to go above and beyond the minimum Reg CC suggestions without any special equipment.

None at all. “Endorse” is the form of the word in common use, while “indorse” is the archaic form found occasionally in legal documents, etc. The two are otherwise completely interchangeable.

Does the endorsement guideline affect liability for all types of fraud, or only duplicate deposits?

The endorsement indemnity rule strictly concerns duplicate deposits. It is “not applicable when the loss is the result of an alteration of an item, or a counterfeit item.”

Do the Reg CC endorsement guidelines apply to all check images, or just those accepted through RDC?

Although remote deposit capture is mentioned extensively, the rule applies to “duplicate deposits.” Theoretically, this could mean any check image. In practice, though, if the check was not deposited using RDC, the bank should already have the original paper document in its possession, rendering this a moot point.

It’s possible to imagine extremely unlikely situations that are not addressed by the rule – such as a teller error in which the original check was handed back to the customer. However, these would be so rare that there is little value in speculating about them.

Does a virtual endorsement meet the liability standards in Reg CC?

No. The rule is intended to address misuse of the paper document after an image-based deposit; therefore, the endorsement has to be on the paper. Adding markings to the image after the fact are only useful for your own internal controls.

It’s worth mentioning that, if your bank currently uses virtual endorsement for checks scanned at the teller window, it’s probably all right to keep doing that. Since the paper check is in your possession, it doesn’t much matter what happens after that. Each bank has its own policies about what type of endorsement is required for teller deposits (including ATM deposits), and we don’t see much changing about this.

How is mobile check capture affected by the Reg CC endorsement changes?

It’s affected in the same way as desktop check capture – the paper document has to be physically endorsed in order to avoid liability concerns. There’s no printer on a mobile phone, so the endorsement has to be written on the check by the customer. Most banks with mobile RDC already have this as a required step, so we don’t foresee major changes in this respect. Some check printers are also including a pre-printed checkbox on the back of the document with language that the check has been deposited electronically.

Will I need to replace check scanners because of the new regulations?

Not necessarily. It’s true that the main segment of check capture affected by the Reg CC change will be desktop deposit using non-Inkjet scanners. (Mobile deposit should remain largely unaffected, as mentioned in the previous section.)

While replacing scanners already deployed in the field would be one option, keep in mind that endorsements are not required under the new rule – just suggested as a way to avoid liability. If a bank is confident that the occasional loss from duplicate deposits is less of a problem than replacing hardware, it is free to keep using RDC without endorsements as long as it is comfortable accepting the risk. The overall occurrence of duplicate-deposit fraud tends to hover at about 3 out of every 10,000 items, so the calculations are not too difficult to make.

Other intermediate options would include replacing non-inkjet scanners only for the highest-risk or highest-volume customers; replacing non-inkjet scanners as they reach the end of life naturally; or, when possible, upgrading certain non-inkjet models with an endorser. It would also be possible to require a handwritten endorsement just as in mobile deposit – although we imagine this would be hugely unpopular in terms of its impact on the customer experience.

One best practice to minimize future risk, while keeping short-term costs and disruption reasonable, would be for the bank to “grandfather” non-inkjet scanners already in use, but to only issue inkjet-enabled models to all customers who are ordering new or replacement devices going forward.