A duplicate deposit occurs when a someone deposits the same check twice, or deposits it and then also attempts to cash it. This is typically done by first depositing an image of the the check electronically, then attempting to deposit or cash the original paper check separately. This practice was not possible for members of the general public until the introduction of electronic services like remote deposit capture or mobile deposit, since before that time, depositing a check required transferring physical possession of the original paper document to the bank.

When done intentionally, duplicate deposits are a form of check fraud. In other cases, they can happen accidentally; for example, if someone deposits a check at an ATM without realizing their spouse already deposited it using a mobile app.

In cases of deliberate fraud, the perpetrator would most commonly use two different financial institutions — or a bank and a non-bank entity such as a check-cashing business — rather than trying to deposit the check twice at the same bank. Since the sharing of information between different financial institutions is not immediate, this would lessen the chances of the fraud being discovered right away. Fraudsters would also typically try to get as much of the funds in cash up front as possible, by immediately withdrawing the maximum available amount from the account into which the check was electronically deposited, and cashing the paper document for its full value. This would minimize the amount of money that the bank could recover later by reversing the transaction if the fraud was discovered.

While duplicate deposit fraud saw a surge in activity in the early 2010s as mobile deposit became widespread, banks have since eliminated much of it by adding policies such as requiring restrictive endorsements on electronically deposited checks, or by implementing lower limits on deposit values and on immediate funds availability. Sharing of information across the industry has also become much faster, enabling banks to catch duplicates before funds are credited or paid out.

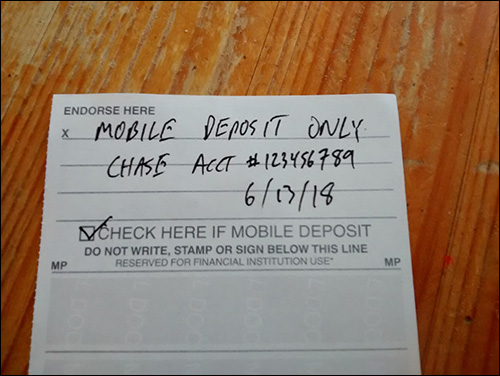

Changes to Reg CC, the Federal Reserve Bank’s rules regarding check clearing and settlement, clarified that in cases of duplicate deposit, the bank of first deposit that received an electronic copy of the check would be liable for any subsequent fraud losses, unless a restrictive endorsement was visible on the check image. That practice makes it unmistakable to any second (or third) entity receiving the check that it has already been deposited. Since then, endorsement requirements for mobile check deposit have become nearly universal across the industry, greatly reducing the opportunity for duplicate deposit fraud.