Last week, I walked up to the counter at the local grocery-store bank branch and handed in a $3.00 mail-in rebate check to deposit. But whatever the teller did, she couldn’t get it to scan correctly – probably because it had torn off unevenly along the perforated bottom edge, so it would not sit level in the scanner track.

After a few tries, the manager came over to help; she took out the check, then put it back in the feeder upside-down and scanned it again.

Pop quiz – what should my reaction have been?

a) “NONONONONOOOOO – don’t ever do it that way!”

b) “Nice job, that’s exactly what you’re supposed to do!”

Had enough time to think it over? Well, to be fair, neither answer is correct 100% of the time, but if you picked “B,” you’re on the right track.

What was going on here? At the bottom of each check, the account number and the bank’s routing number are printed in magnetic ink (known in the industry as the MICR line). Inside the scanner, a magnetic read head sits at the bottom of the track to read that information as the check goes past. Since the MICR line is in almost exactly the same place on every check, the read head is only designed to pick up the magnetic signal from the very bottom; in fact, we wouldn’t want it to pick up anything else.

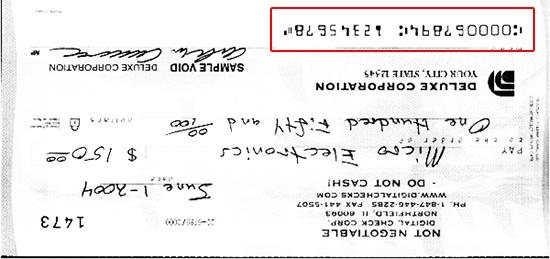

Put a check in the wrong way? Our scanners will look for an upside-down MICR code – but won’t be able to read the magnetic ink itself

But in this case, the check was not sitting level, so part of the MICR line was tilted up and above the magnetic read head. That caused the scanner to only pick up part of the account information, generating a “can’t-read” error.

Why did it fix the problem when the manager scanned the check upside-down? Basically, because she fooled the scanner into thinking she’d made a mistake, and took advantage of its failsafes to fix the problem.

Believe it or not, people put checks into the scanner upside-down all the time by accident. So if one of our devices detects no magnetic ink at the bottom, the first thing it does is use optical character recognition, or OCR, to look at the top of the check for an upside-down MICR line. (Technically, it flips the image in memory and checks the bottom for right-side-up MICR, but it’s all the same as far as we’re concerned here.) If it finds the MICR printing, it treats it as a check and displays the flipped-over image; if it still detects nothing, it displays the original image, probably along with an error message.

It’s pretty easy to recognize an upside-down check, because MICR printing in the U.S. and Canada uses a distinctive font called E13B that’s rarely used for anything else. So usually, applying optical detection gives you the right numbers and you can send the check through like normal. But – and this is a big BUT – if something happens that throws off the optical recognition engine, you run the risk of having a serious error like an incorrect account number if you just send the check through. This could be caused by anything from a smudge or writing in the MICR area, to a check with an intense background that interferes with the contrast and light levels for the rest of the document.

MICR recognition, assuming there’s MICR to read and it’s printed correctly, is nearly perfect – think 99.999%+ accuracy rates – but while OCR is also very good, there are a lot more things that can “fool” it. So it’s better to be on the safe side and verify the MICR line on any upside-down checks with a manual inspection.

In fact, with banks reporting that “critical errors” like incorrect account numbers cost anywhere from $15 to $30 each to resolve once the check goes through, if visual inspection catches a mistake in even 1 out of every 1,000 upside-down scanned checks, it more than makes up for the few seconds needed to take a look.

The “bottom line” (pun intended): DO try flipping your check upside-down if it won’t scan – but ALWAYS double-check it afterward.